SK Hynix Becomes Asia's 3rd-Largest Co. on HBM Supercycle

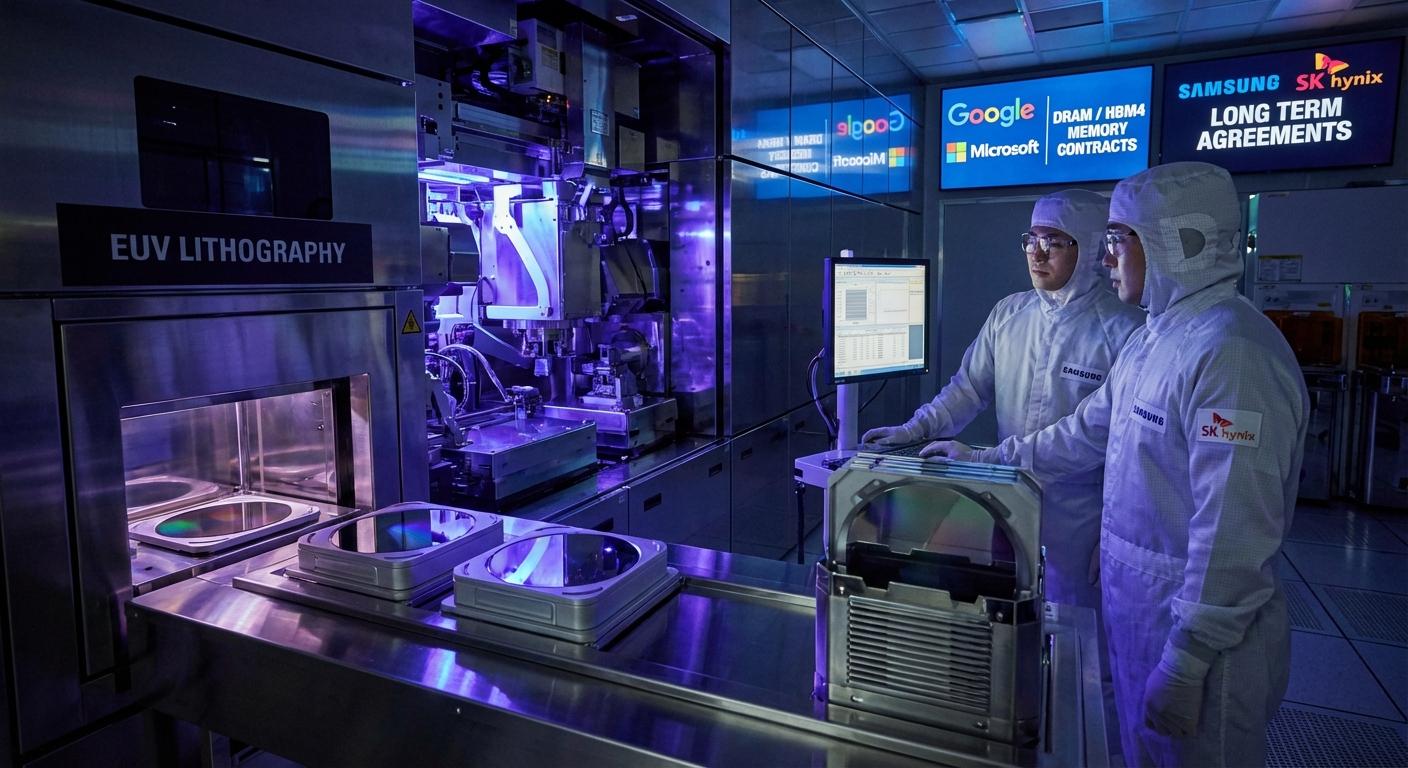

MAY 27, 2026 — SEOUL, SOUTH KOREA. SK Hynix shares closed at an all-time high of 1,680,000 won this week, lifting the Korean memory maker into the position of Asia's third-most-valuable listed company on a rally of 186% year-to-date, according to CNBC. Microsoft, Google, and Amazon have separately offered to underwrite further capacity expansion as 2026 high-bandwidth memory inventory is already sold out, in what is now the most aggressive customer-financed buildout in memory-industry history.

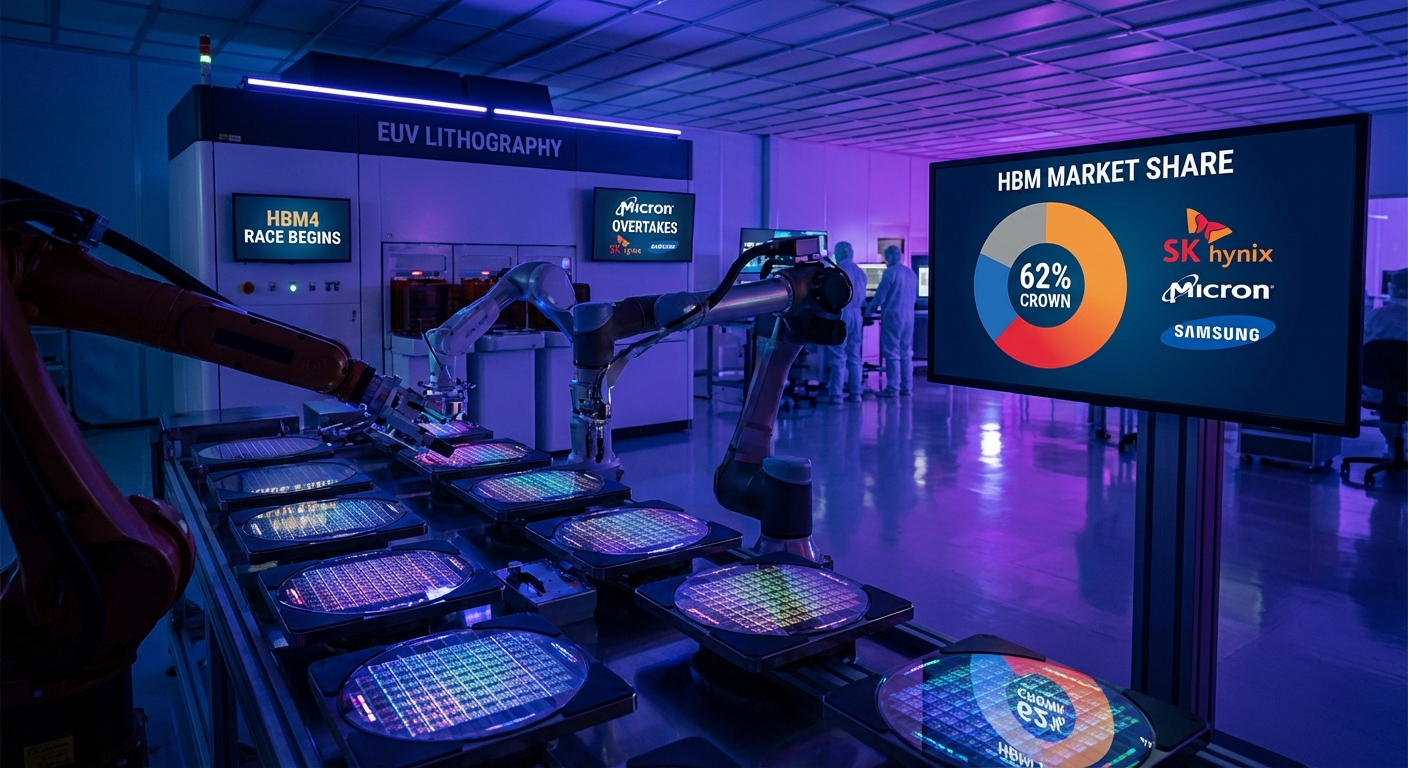

The fundamentals justify the rerating. SK Hynix posted a Q1 operating profit of 37.6 trillion won on an operating margin of 72% — a level that briefly exceeded Nvidia's gross-margin performance in the same quarter and reflects the structural pricing power memory now holds at the AI training tier. The company controls roughly 61% of global HBM revenue, and CNBC reports more than 95% of sell-side analysts now carry a BUY rating on the stock, with several upgrading price targets above 2,000,000 won on the back of HBM4E qualification wins at Nvidia, AMD, and Broadcom. The Q1 result also reflects a near-complete decoupling from the legacy DRAM and NAND cycles that historically governed memory valuations — HBM now accounts for the dominant share of operating profit despite remaining a minority of bit-shipment volume.

The hyperscaler-funding offer is the structural news inside the share-price story. Ad-hoc News reports that the three top US cloud operators have approached SK Hynix with prepayment and equity-style financing proposals to accelerate the M15X and Cheongju expansions ahead of the company's organic capex schedule. The 2026 memory market is now sized at $440 billion, and TrendForce notes that Samsung's custom HBM4E program — its primary lever to catch up — is not slated for volume until mid-2026, leaving SK Hynix as the de facto monopoly supplier for the next two HBM generations. FX Leaders adds that the company's 3 trillion won share buyback announced earlier in May has further tightened float at exactly the moment passive index demand is rising.

The customer-financing model carries its own consequences. Prepayment arrangements lock SK Hynix into multi-year delivery commitments at negotiated prices that may sit below the spot peaks the next 18 months could deliver, and equity-linked structures hand a portion of the cycle's upside to the buyers funding the buildout. Against that, the alternative — building 2026 through 2028 capacity solely from operating cash flow — would force SK Hynix to either delay expansion or take on incremental debt at a moment when capex intensity across the memory industry is already at historic highs. CNBC's separate analysis argues this cycle no longer fits the traditional memory boom-bust template precisely because the demand side is now contractually pre-committed, not speculative.

The competitive landscape reinforces the rerating. Samsung's 30% HBM share is concentrated in older HBM3 generations rather than the HBM4 and HBM4E SKUs Nvidia, AMD, and Broadcom now require, and Micron's HBM ramp — while accelerating — still trails SK Hynix by at least one full process generation. That leaves SK Hynix as the only supplier qualified at every leading AI-accelerator customer for the 2026 and 2027 product cycles. FX Leaders calculates that even if Samsung's custom HBM4E ramps cleanly into the second half of 2026, the unit-volume gap will not close meaningfully before 2028, sustaining SK Hynix's pricing leverage through at least two more quarters of guidance upgrades.

The combination of customer-funded capex, single-supplier leverage on the most constrained AI input, and Nvidia-grade margins has rewritten what a memory company can be worth. The risk now flips: if SK Hynix accepts hyperscaler money, the cycle's terminal value rises but the customer base gains structural pricing leverage over the next downturn. Either way, the 2026 memory market is no longer cyclical in any traditional sense, and the rally is — by analyst consensus — only at the halfway mark.

Sources

CNBC, TrendForce, FX Leaders, Ad-hoc News